annuities

← Back to Annuities hubFixed Annuity Surrender Charges Explained

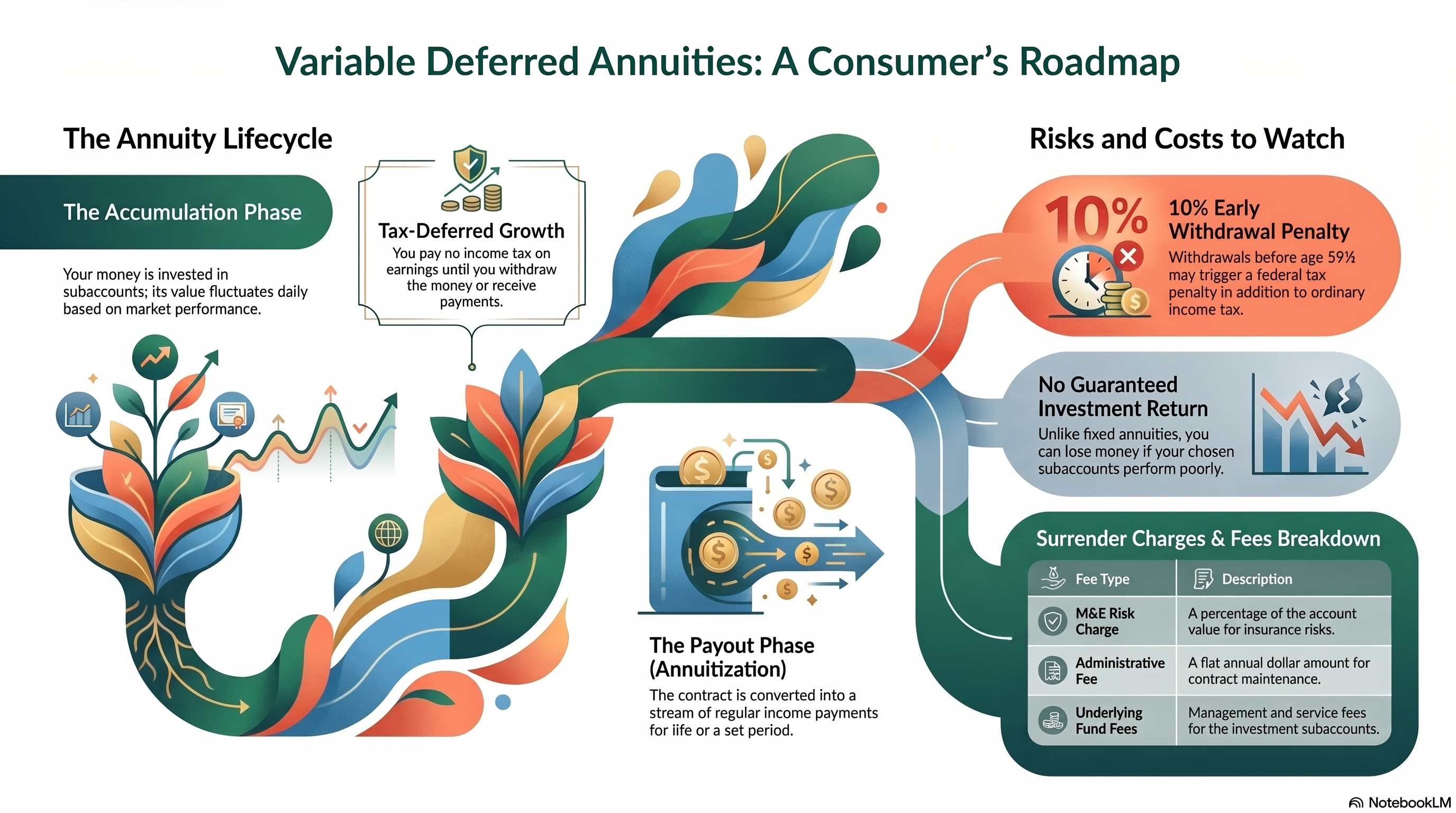

Surrender charges are one of the most important contract terms because they can limit access to money in early years.

Use this guide to understand how surrender schedules work, when penalties may apply, and how to evaluate liquidity before purchase.

Fixed Annuity Surrender Charges Explained - Video Brief

A practical walkthrough of surrender schedules, free withdrawals, and MVA trade-offs.

Video placeholder

This page is ready for an embedded video when the final asset is available.

What surrender charges are

A surrender charge is a fee that may apply when withdrawals exceed contract limits during a defined surrender period.

They are designed to discourage early exits from long-term contracts.

How surrender schedules are structured

Most contracts use a declining schedule where charges decrease over time.

The highest percentages are often in earlier years and step down annually.

- Always confirm the exact schedule in your contract illustration.

- Do not assume one carrier's schedule matches another.

Free-withdrawal provisions

Many contracts allow a limited annual penalty-free withdrawal amount.

Rules vary by contract and may include waiting periods or conditions.

What is an MVA and why it matters

Some annuities include a market value adjustment (MVA), which can increase or decrease withdrawal value depending on interest-rate changes.

MVA can materially affect surrender outcomes, especially in volatile rate environments.

Liquidity planning before purchase

- Keep emergency reserves outside long-term annuity contracts.

- Match contract duration to your expected cash-flow timeline.

- Review rider options and access rules before signing.

- Stress-test what happens if you need funds earlier than planned.

Practical takeaway

Surrender charges do not automatically make a contract bad, but they do require careful fit analysis.

If access flexibility is a priority, compare alternatives before committing.

Frequently asked questions

Do all fixed annuities have surrender charges?

Many do, but structures vary. Review your contract's specific surrender schedule and liquidity terms.

Can I withdraw any money without penalty?

Often yes, through free-withdrawal provisions, but limits and eligibility conditions vary by contract.

Is an MVA the same as a surrender charge?

No. An MVA is a separate adjustment that can raise or lower withdrawal value based on interest-rate movements.

How do I reduce surrender-charge risk?

Maintain liquid reserves, align contract terms to your timeline, and review all withdrawal rules before purchase.

Helpful calculator

Use this educational calculator to pressure-test planning assumptions.

Annuity Payout Calculator →Download guide

Get a practical checklist to review options with more confidence.

Annuity Questions Checklist →Surrender Charge Review Worksheet

Use a checklist to compare surrender schedules, MVA terms, and liquidity fit before buying.

Related articles

annuities

Can You Lose Money in a Fixed Annuity?

Fixed annuities are designed for stability, but retirees should still understand contract and planning risks.

annuities

Fixed Annuity vs CD: What Retirees Should Compare

Fixed annuities and CDs both offer stability, but they serve different retirement income goals.

annuities

How Do Fixed Annuities Work?

Fixed annuities are insurance contracts with defined terms that can support retirement income planning.

This website provides educational information only and does not provide personalized financial, tax, legal, or Medicare plan advice. Annuity guarantees are backed by the claims-paying ability of the issuing insurance company. Medicare plan availability, costs, and benefits may vary by state, carrier, plan, and personal circumstances. Not connected with or endorsed by the U.S. government or the federal Medicare program.