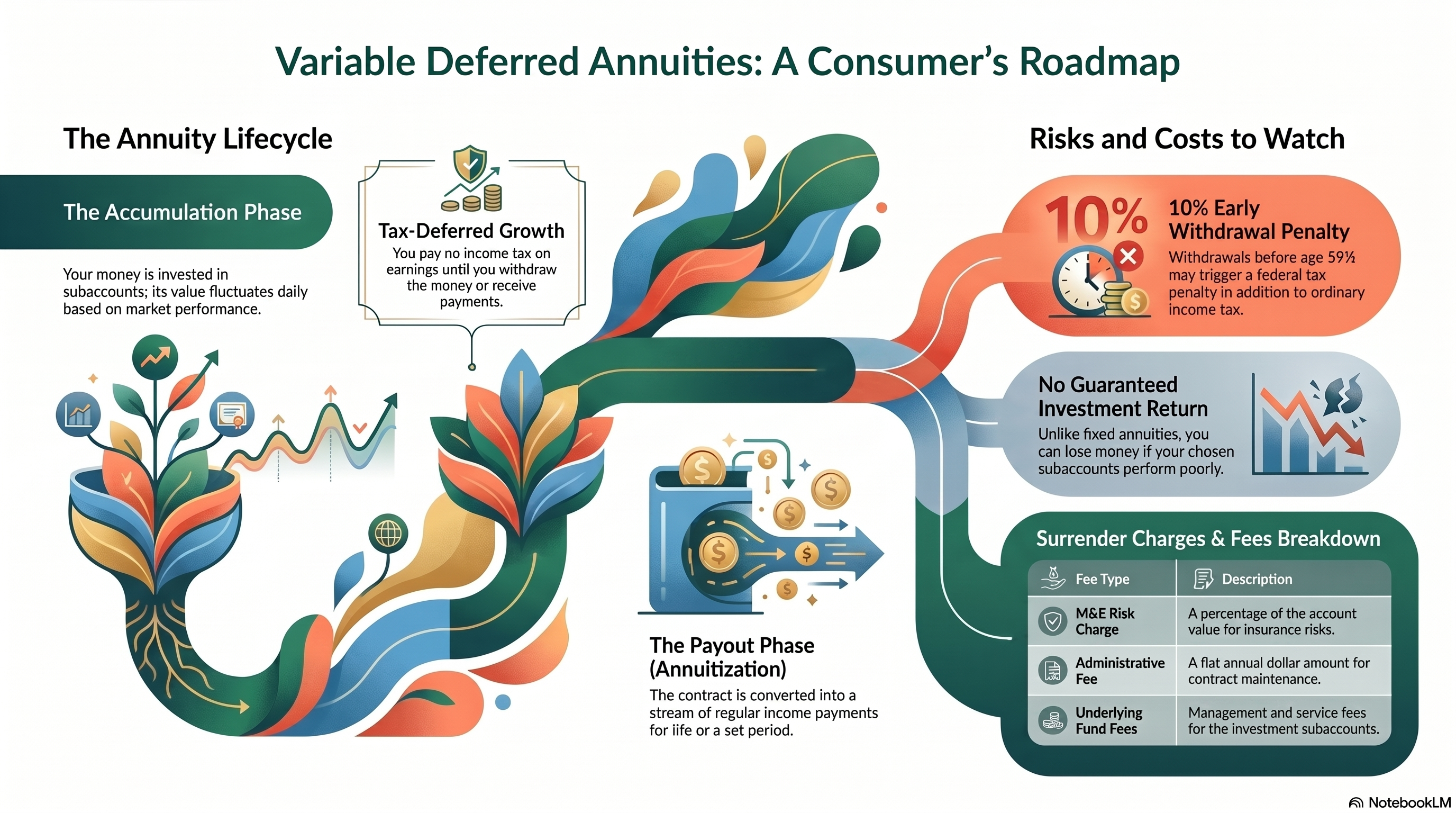

annuities

← Back to Annuities hubWhat Happens If an Insurance Company Fails?

Insurer insolvency is uncommon, but understanding the process helps retirees evaluate annuity risk with clearer expectations.

This guide explains what can happen if an insurer fails, how state guaranty associations may respond, and why prevention starts with carrier due diligence.

What Happens If an Insurance Company Fails? - Video Brief

A plain-English guide to insurer insolvency context and state guaranty association limits.

Video placeholder

This page is ready for an embedded video when the final asset is available.

How annuity guarantees are backed

Annuity guarantees depend on the claims-paying ability of the issuing insurance company.

That is why carrier quality is a core part of product selection, not just contract features.

If an insurer becomes insolvent

State insurance regulators step in to supervise the insolvency process.

The goal is typically to protect policyholders through transfer, rehabilitation, or claim administration mechanisms.

Role of state guaranty associations

State guaranty associations may provide protection for eligible contracts within state-specific limits.

Coverage limits are not identical across states and should be verified directly.

- Coverage is generally limited and subject to conditions.

- These associations are a safety framework, not a planning strategy by themselves.

Why insurer selection still matters

- Stronger carriers may reduce insolvency risk in the first place.

- Independent ratings can help compare financial strength trends.

- Diversification and contract fit can reduce concentration risk.

Questions to ask before purchase

- What are the insurer's current ratings and outlook?

- What are your state's guaranty association limits for annuities?

- How much liquidity do you retain outside the contract?

- How do surrender terms affect flexibility if plans change?

Practical takeaway

Use guaranty association information as a backstop reference, not as the primary reason to choose a contract.

Prioritize financially strong insurers, clear contract terms, and liquidity planning aligned to your goals.

Frequently asked questions

Do I automatically lose my annuity if an insurer fails?

Not automatically. Regulators and state frameworks often manage transitions, but outcomes depend on contract details and state limits.

Do state guaranty associations cover everything?

No. They may provide protection up to specific limits, which vary by state and product category.

Can guaranty associations replace insurer due diligence?

No. They are a backstop and should not replace reviewing carrier financial strength before purchase.

What is the best risk-management approach?

Review insurer ratings, contract terms, liquidity needs, and concentration exposure before committing funds.

Helpful calculator

Use this educational calculator to pressure-test planning assumptions.

Fixed Annuity vs CD Calculator →Download guide

Get a practical checklist to review options with more confidence.

Annuity Questions Checklist →Carrier Strength Due-Diligence Checklist

Get a practical list of insurer, contract, and liquidity checks before finalizing an annuity decision.

Related articles

annuities

Are Fixed Annuities FDIC Insured?

Fixed annuities are not FDIC-insured bank products, so protection rules differ from CDs and savings accounts.

annuities

Can You Lose Money in a Fixed Annuity?

Fixed annuities are designed for stability, but retirees should still understand contract and planning risks.

annuities

Fixed Annuity vs CD: What Retirees Should Compare

Fixed annuities and CDs both offer stability, but they serve different retirement income goals.

This website provides educational information only and does not provide personalized financial, tax, legal, or Medicare plan advice. Annuity guarantees are backed by the claims-paying ability of the issuing insurance company. Medicare plan availability, costs, and benefits may vary by state, carrier, plan, and personal circumstances. Not connected with or endorsed by the U.S. government or the federal Medicare program.